It is really important to keep in mind the difference between claims or value judgments (normative) and statements of reality (postive) especially when evaluating an argument. Arguments rest on premises and draw to conclusions based on logic. That logic should take you from the facts to the conclusions and you should constantly be evaluating whether there is another alternative to the proposed logic. This is a life skill not just a skill relating to economics. If you have further questions PLEASE come see me.

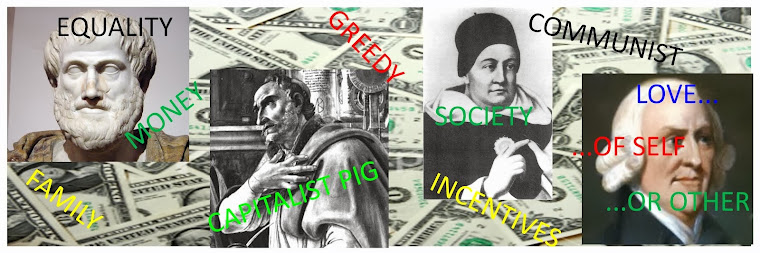

Secondarily, identifying those normative statements which may be intended to "frame" an argument or discussion by taking certain tradeoffs off the discussion table are important. So, for example, this often occurs when the words 'fairness,' 'greed,' or 'exploitation' are used. It is not that none of those things may occur but rather that we should be sceptical that those words will not merely be used to avoid a conversation about the opportunity cost of an action. The best current examples I can think of come from sequestration. So many of the arguments against sequestration go something like: you can't cut funding from there itll cost lives! The idea being that you should never do something which may, however indirectly, result in death. Of course what often gets left out is that funding that project may cost lives in other areas, so that spending money on airline safety might actually result in fewer dollars allocated to vehicular safety and actually result in far more deaths. In any case, we need to be aware of this.

For next time, in addition to your paper, write out two questions you would put on the final and answer them. Your final 15 IP points will be based on this submission.

Secondarily, identifying those normative statements which may be intended to "frame" an argument or discussion by taking certain tradeoffs off the discussion table are important. So, for example, this often occurs when the words 'fairness,' 'greed,' or 'exploitation' are used. It is not that none of those things may occur but rather that we should be sceptical that those words will not merely be used to avoid a conversation about the opportunity cost of an action. The best current examples I can think of come from sequestration. So many of the arguments against sequestration go something like: you can't cut funding from there itll cost lives! The idea being that you should never do something which may, however indirectly, result in death. Of course what often gets left out is that funding that project may cost lives in other areas, so that spending money on airline safety might actually result in fewer dollars allocated to vehicular safety and actually result in far more deaths. In any case, we need to be aware of this.

For next time, in addition to your paper, write out two questions you would put on the final and answer them. Your final 15 IP points will be based on this submission.

{kind=link}